Leasing a car is a legal contract between a lessee and a leasing company that owns the vehicle. Essentially, you are agreeing to pay for the exclusive use of a vehicle under certain terms that include:

- A maximum accumulated mileage

- A regular payment model

- A set length of time

- Returning the vehicle in good condition

There can be several reasons that you may want to end your lease early.

- A third party wants your car

- You lost your job

- You may be moving overseas

- You may no longer need the vehicle due to the close proximity of home to your workplace

- Your vehicle needs have changed such as the birth of a child

Whatever the situation, you may be able to break your lease agreement. Before you proceed with breaking your lease agreement, you need to be aware of the terms of your lease, including any penalties you will owe, any lease payout fees, your eligibility to transfer your lease, and any ongoing liability you may have for the remaining term of your lease.

Method 1 of 4: Contact your lease provider

Step 1: Know your lease terms. Whether you’ve leased your vehicle through a car dealership or through a leasing agency, contact the leaseholder to find out the terms of your lease.

You can also read through your lease contract where the terms are clearly explained.

Ask specifically if you are eligible to transfer your lease and the terms thereof.

Step 2: Keep track of the fee. Write down the applicable fee for your situation.

If you are unsure which avenue you will be taking to get out of your lease, write down every possibility.

Specifically request the optional lease buyout amount that remains at the end of your lease.

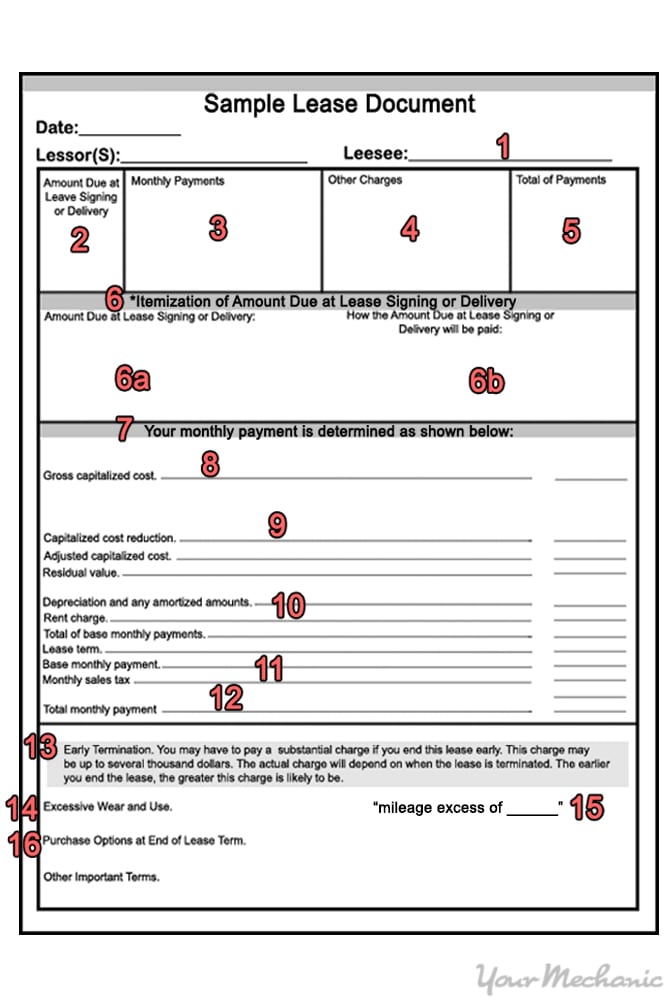

1 - Name

2 - Total amount due at lease signing

3 - Calculation of monthly payments

4 - Disposition or other fees

5 - Total payment (at end of lease)

6 - Payment breakdown

6a - Total amount due at lease signing

6b - Total amount due at lease signing

7 - Monthly payment overview

8 - Gross cost

9 - Rebates or credits

10 - Additional charges, monthly payments, total monthly payments, and lease term

11 - Tax

12 - Total monthly payment

13 - Warning about early termination

14 - Charges for excessive wear and tear

15 - Purchase option price

16 - Purchase option fee

Step 3: Weigh your options. If the fee is several thousand dollars to break your lease, consider keeping the vehicle in your possession, making the most of the situation.

For example, if you have a monthly payment of $500 and 10 months remaining on your lease and the fee to break your lease is $5,000, you’ll be paying the same amount whether you are driving your car or breaking the lease.

Method 2 of 4: Transfer your lease

Transferring your lease is the easiest way of being released from your legal obligation on your lease. In this method, you find another person willing to be the lessee for the vehicle, relieving you from your obligation. Be prepared to provide an incentive for your lease takeover such as leaving your damage deposit for the new lessee.

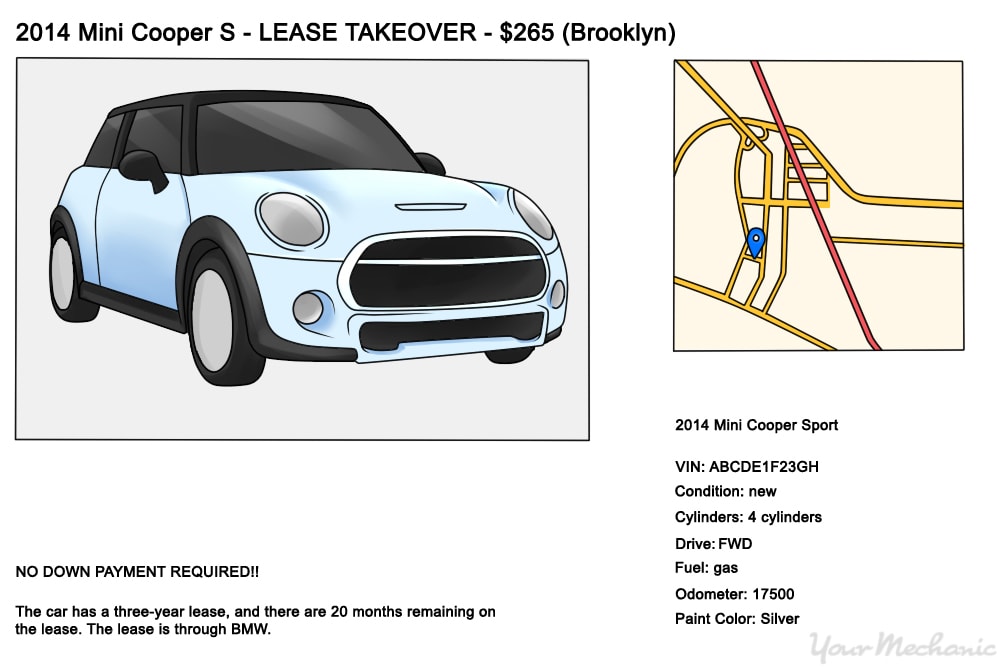

Step 1: List as lease takeover. List your vehicle as a lease takeover in car ads.

Using print ads in your local newspaper, buy-and-sell publications, and online marketplaces such as Craigslist, post your vehicle requesting someone to take over your lease payments.

Use specific information that informs the reader of the remaining term of your lease, the monthly payment, any applicable fees, the lease buyout at the end, the mileage, and the vehicle’s physical condition.

- Tip: There are online services such as SwapALease and LeaseTrader which specialize in matching those wishing to break their lease with potential lease takeover clients. They charge a fee for their service which may be well worth it as they take care of all the legwork transferring the lease. The clientele are vetted and ready to take over your lease, making your part in the process much simpler.

Step 2: Be professional. Respond to inquiries quickly and arrange to meet an interested party.

If the potential lessee would like to proceed with taking over your lease, arrange a time that both parties can meet at the leasing company. Make an appointment for the lease takeover.

Step 3: Fill out your paperwork. Complete the necessary paperwork to transfer the lease to the new party. This will include the leasing company running a credit check on the new lessee.

If the new lessee checks out, sign the contract release, fill out your title transfer, and cancel your vehicle insurance and registration.

Tip: When transferring your lease, bring all your car keys, owner’s manual, and vehicle documents with you to make the transfer smooth and simple.

Warning: Some lease companies include a clause that keeps the original lessee liable for the payments if the person who assumed the lease defaults. This type of liability is known as post-transfer liability and, though it is only used in approximately 20 percent of leases, you should be aware of your remaining obligation until the lease is complete. Post-transfer liability is mainly used by luxury car companies such as Audi and BMW.

Method 3 of 4: Buy out your lease

Transferring your lease may not be the best option for you in some instances such as:

- A purchaser wants to buy your car

- The potential lessee has poor or insufficient credit to take over the lease

- You have positive equity in your leased vehicle

- You want to own your car outright without payments

- Your car has excessive mileage, damage, or wear

- Your lease has a post-transfer liability

The process is the same regardless of your purpose for buying out your lease.

Step 1: Calculate the cost of the buyout. Determine the total cost of buying out your lease.

Consider all the factors including the buyout amount, additional fees to the leasing company, title transfer costs, and potential taxes you will owe.

For example, if your lease buyout is $10,000, the lease termination fees are $500, the title transfer cost is $95, and you pay 5% tax on the lease buyout ($500), your total cost to buy out your lease is $11,095.

Step 2: Arrange financing. Unless you’ve come into a substantial amount of money, you will need to arrange a loan through a financial institution to buyout your lease.

Step 3: Pay off the deficit. Pay the leasing company the price owed to buyout your lease.

If it is through a car dealership, you will pay sales taxes on the sale amount at the dealer.

If you are planning to sell your car, you can now do so.

Method 4 of 4: Turn in your lease early

If you are unable to transfer your lease or buy it out, you can turn it in early. This situation comes with notoriously high penalties, often equivalent to the remaining lease payments as a lump sum.

Before turning in your lease early because of financial difficulty, check with your lease provider to find out if there are any other options available such as a skip-a-payment option. If you’ve exhausted all other options, turn in your lease early.

Step 1: Turn in your lease. Contact your lease provider to arrange an appointment to turn in your lease.

Step 2: Clean out your vehicle. Remove all your personal belongings, and make sure the car is in a presentable state.

To prevent additional charges, have the car professionally detailed if there are excessive stains or soiling to the interior or if there are scratches on the exterior.

Step 3: Provide the necessary items at your appointment. Bring all your keys, owner’s manual, and documentation to your appointment. You will be leaving your car behind.

Arrange alternate transportation home from the leasing company.

Step 4: Fill out the forms. Complete the forms required with the lease provider.

The lease provider will do everything in their power to try to keep you in your lease. Work with them, exploring every viable option if you would prefer to keep your leased car.

Step 5: Turn over the vehicle. Turn over your car, your keys, and the books.

If you choose not to turn in your lease early and default on your payments, it may happen involuntarily. Your car will be repossessed by the leasing company to recoup their losses and to recover their asset. This is the worst scenario possible as your credit score will suffer and a repossession on your credit report may prevent you from being able to finance or lease anything for up to seven years.