When you lease a vehicle, you agree to a set term that you will make lease payments on a vehicle. Leases can often be an excellent option to car ownership because after the term is complete, you can simply return the car to the leasing company without the hassle of finding a buyer, negotiating, or certifying your vehicle.

What happens if you can no longer make your lease payments or you wish to get a different vehicle? As a lessee, you are responsible to make your lease payments until the term is expired, unless you are able to transfer the lease to another party or break your lease.

It might not be as difficult as you think to sign your lease over to someone else as there are plenty of people who are interested. Some of these reasons include:

- They only want a car for a short period of time

- They don’t have the money for a down payment on a new car

They might need a different kind of car in a hurry (for example, if someone just had a baby and now needs a minivan)

Note: When you transfer your lease or break your lease agreement, expect that there will be a financial penalty. You will lose any equity you’ve built in the vehicle or may have to pay huge lease termination fees.

Method 1 of 3: Transfer your lease

Lease agreements are a great deal easier to transfer directly to another party than a loan. Lease agreements are a relatively simple contract between the lessee and lessor. As long as the terms of the lease are met, and the lessee can prove that they pose minimal threat to breaching the terms of the agreement, leasing companies are typically open to transfer the lease to another party.

It’s beneficial for someone to take over a lease in many situations. Because numerous lease payments have already been made, the length of the lease term is reduced so the commitment is shorter. As well, if the residual amount on the lease is small it can be quite attractive to buyout the lease at the end, resulting in the possibility of a great buy.

Step 1: Determine your eligibility to transfer your lease. Not all leases are able to be transferred.

Check with your leasing company to determine if you are able to transfer your lease to someone else.

Step 2: Find a party to take over your lease. You may know a family member, friend, or coworker who wants to take over your lease.

If you don’t have someone who wants to take it over, use social media, print advertisements, or online services to find a new lessee.

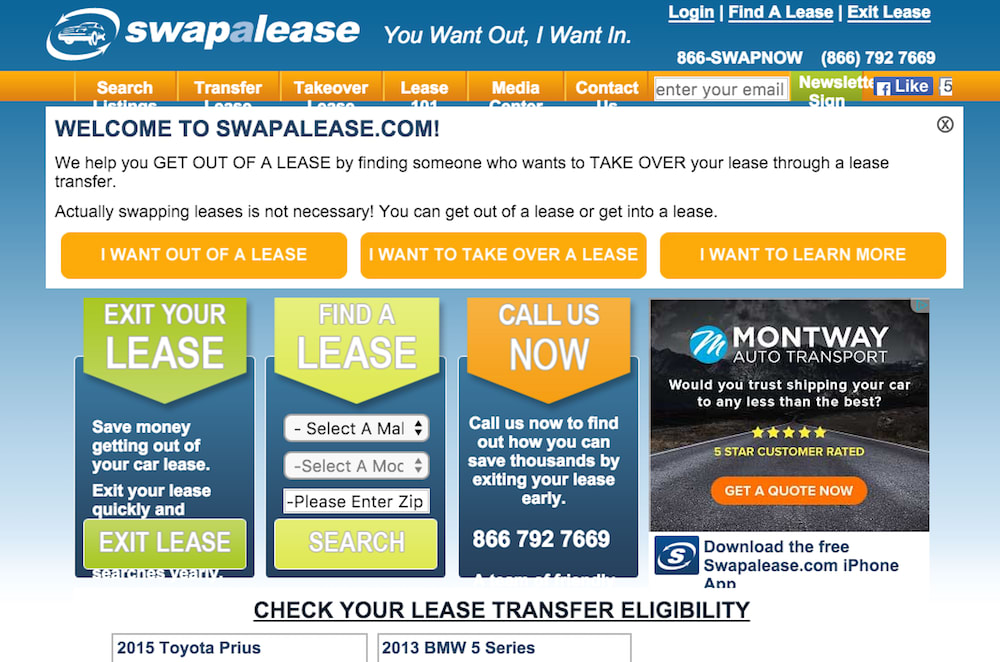

Services such as SwapaLease and LeaseTrader help match those looking to get rid of their lease with potential lessees. A fee is charged to list the ad, and a commission is charged once the lease is taken over. The commission charged is dependent on the agreement.

Step 3: Transfer the lease. You will need to officially transfer the lease to the lessee. If you are using an online service to transfer your lease, they will take care of the necessary paperwork to complete this step.

If you have found a new lessee on your own, contact the leasing company with your new lessee.

The new lessee will need to submit to a credit check in order to be eligible to take over the lease.

The leasing company will release the title lien once the new lessee is approved and a contract has been completed.

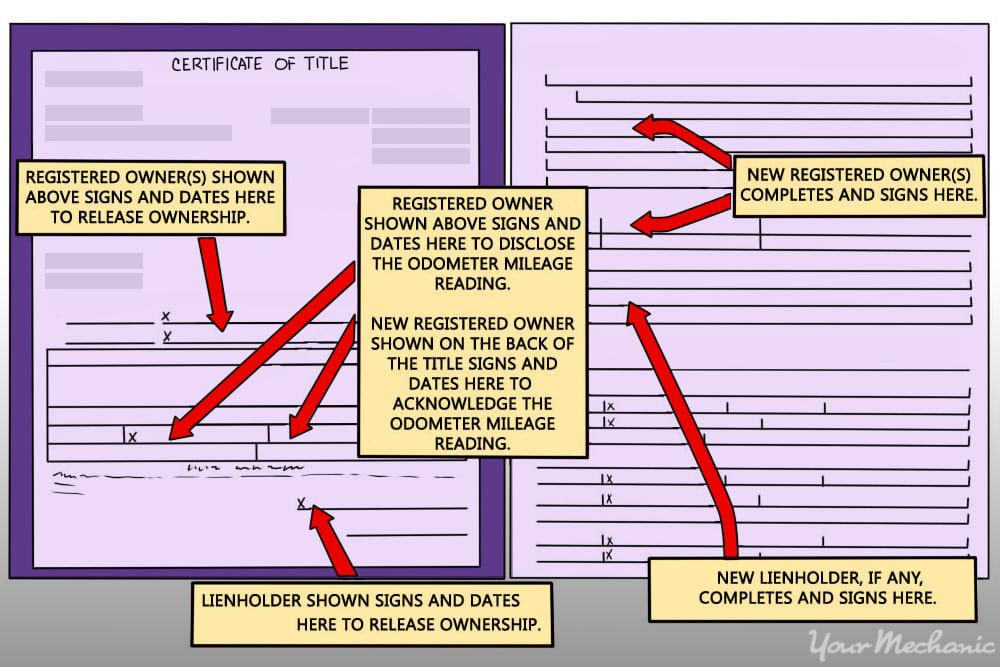

Step 4: Transfer the title. Once the lease has been transferred, complete a title transfer with the new owner.

Method 2 of 3: Lease your vehicle to a friend or family member

If your lease isn’t eligible to be transferred or you aren’t able to sell your car due to negative equity, you can effectively lease your car to a family member or friend informally. They can pay you for the use of your vehicle while you maintain legal ownership of the car.

Step 1: Find out if it’s legal in your state: In many states, it is not legal to be the primary driver of a vehicle while the vehicle insurance and registration is under another party’s name.

In some states, you may find it is not possible to use this method legally.

Step 2: Find a friend: Ask friends and family members who are looking for a car if they’re interested in taking over your lease.

Step 3: Add their name on the car’s insurance: Depending on the state and the insurer, you may be able to obtain rental car insurance or transfer the vehicle insurance to the vehicle driver while it is in their possession.

Method 3 of 3: Terminate your lease early

If you are unable to find a new lessee and are willing to absorb financial penalties to terminate your lease early, this may be an option for you. Some early lease termination fees are hefty and can be several thousand dollars.

Step 1: Determine terms for early termination. Contact your leasing company to determine the terms for early lease termination.

Check your lease contract as well. The early termination fee will be detailed there. Ford has an online example of the finer points of a lease agreement.

Step 2: Consider benefits and disadvantages. Weigh the benefits and disadvantages of terminating your lease.

The fee could make early termination cost-prohibitive. However, you may need to be released from the contract due to circumstances such as relocation.

Step 3: Complete the paperwork. Complete the termination paperwork with your leasing company including a title transfer.

Cancel your vehicle insurance and registration to finish the transaction.

All in all, there are several options for you to get out of lease if you find this necessary for your circumstances. While the terms of the lease are not very flexible, you can always have the lease transferred to others, or end your lease, by using the methods above.