Leasing a new car is difficult enough without the added trouble of bad credit. A poor credit rating can make leasing a new vehicle a challenge.

While the dealer may have the upper hand thanks to your less-than-stellar rating, it’s important to remember that you do have options. The car leasing experience is definitely going to be more difficult thanks to your credit rating, but it doesn’t have to be impossible, or even unpleasant.

Doing a little homework up front can usually make the process much easier and dramatically increase your chances of reaching a satisfying deal for both you and the dealer.

Let’s look at a few ways to make driving off the lot in your dream car a reality, regardless of your credit rating.

Part 1 of 4: Know what you’re up against

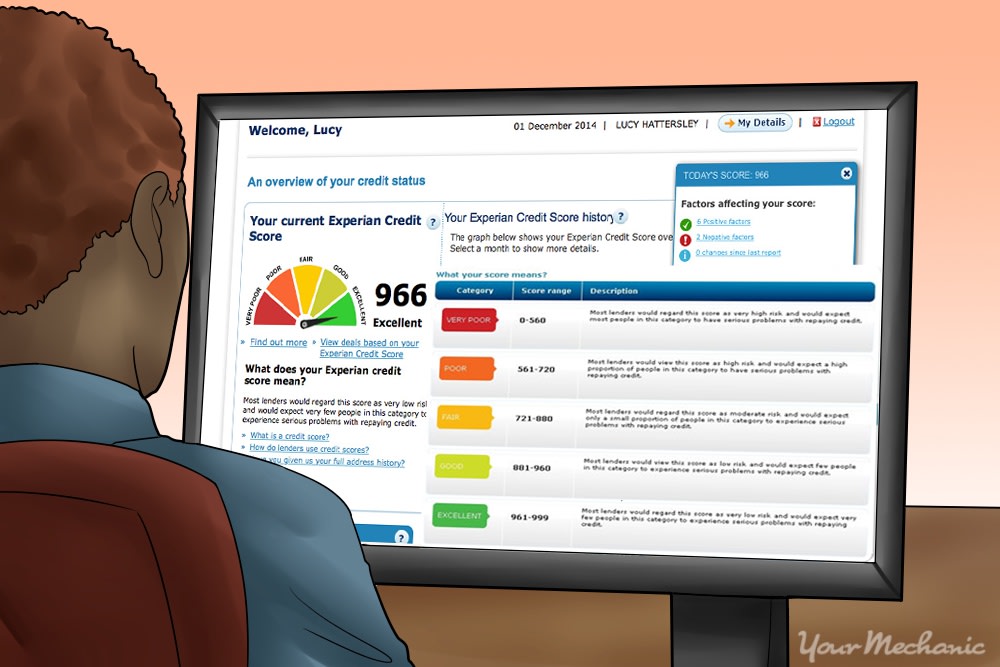

You want to go into the dealership informed. Knowing exactly what your own credit score is eliminates any surprises when you hit the dealer floor. Here is what you need to know about FICO scores:

Free credit report: Everyone is entitled to a free credit report from one of three credit bureaus every year. Contact Experian, Equifax or TransUnion for copy of your report. You can also get a copy at AnnualCreditReport.

What it contains: A credit or FICO score is simply a measure of your creditworthiness. All current and past credit accounts will be detailed in the report. These include credit card accounts, mortgages, and any loans or leases. It will also notate any late or missed payments, bankruptcies, and repossessions.

- Your score is calculated using a proprietary algorithm, so it will vary slightly between credit bureaus. Consider pulling reports from all three agencies to make sure they all have the same data. Carefully review your credit report, and if you discover any errors, immediately contact the reporting agency to get it corrected.

| FICO Credit Score Ratings | |

|---|---|

| Score | Rating |

| 760 - 850 | Excellent |

| 700 - 759 | Very good |

| 723 | Median FICO score |

| 660 - 699 | Good |

| 687 | Average FICO score |

| 620 - 659 | Not good |

| 580 - 619 | Poor |

| 500 - 579 | Very poor |

What it means: Credit scores range from 500 to 850. The median score for U.S. consumers is 720. Scores above 680-700 are considered “prime” and will result in the best interest rates. If your score falls below 660, it will be considered “subprime,” which means you will be paying a higher interest rate on a car lease. Once your score falls below 500, it will be very difficult to get any type of lease.

Only your credit score matters: Car dealers are not going to examine your credit report; they will only pull your score.

Part 2 of 4: How credit affects leasing a car

A low credit score will impact the car leasing experience in a number of different ways. Here are a few ways that your subprime score will make the process a bit more difficult:

Impact 1: Higher down payment/security deposit. Since you are considered a higher risk, the financing company will want you to have more skin in the game. Expect to pay a significantly higher down payment than shoppers with a “prime” credit rating. Most lenders will ask for at least 10% or $1,000 - whichever amount is greater.

Impact 2: Higher interest rate. The best interest rates are reserved for shoppers with the best credit score, so “subprime” buyers are going to pay a higher rate. The interest rate penalty will vary by lender, and this is where shopping your financing around can make a big difference.

Be realistic. A low credit score can definitely affect the amount of car you can lease. Be realistic when shopping for a vehicle, and make sure it is a vehicle that is affordable. Missing payments will only make your credit situation worse.

The car you get approved to lease may not be your dream ride, but once your credit is repaired, you can shop for a new car or refinance it to a lower interest rate.

Part 3 of 4: Find financing and then find a car

The truth is that finding affordable financing is probably going to be more difficult than tracking down an acceptable ride. Consider all options when looking for funding.

Step 1: Call around: While many dealerships will try to get you in the door, many will be honest with you regarding your chances of approval.

In order to get an idea of just how bad your situation is, call a few dealerships, explain your situation, give them a price range you are comfortable with, and simply ask them what your odds are of being approved.

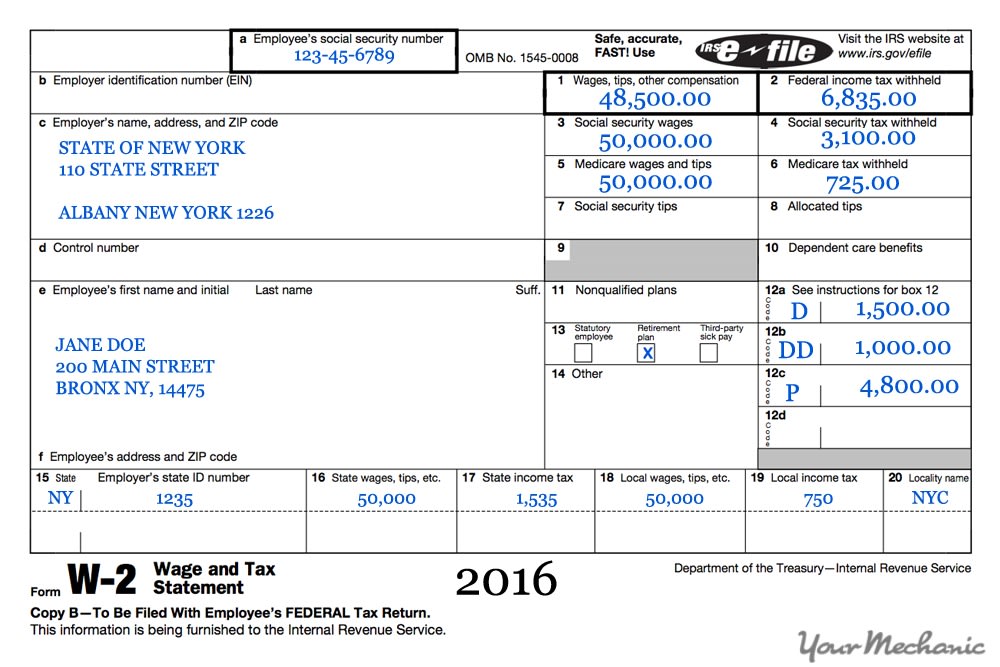

Step 2: Get your paperwork in order: Your credit score is going to raise some red flags, so bring plenty of paperwork with you as back up:

Some paperwork to bring to help verify income includes pay stubs, a W-2, or 1099.

Bring bank statements, utility bills, rental agreements, or a mortgage statement as proof of residency. The longer you have been at your current address, the better.

Step 3: Shop the dealerships: Financing companies rate risk differently, so your goal is to find a financing company that is comfortable with your particular risk factors.

Dealerships will often work with “subprime” lenders that are willing to finance lease deals for poor credit customers.

- Tip: When shopping dealerships, bring your own credit report. Every time a dealer pulls your credit, it dings your score a little. Unfortunately, those dings can add up to major damage if you hit a large number of dealers. Only let a dealer pull your credit if you are serious about making a deal.

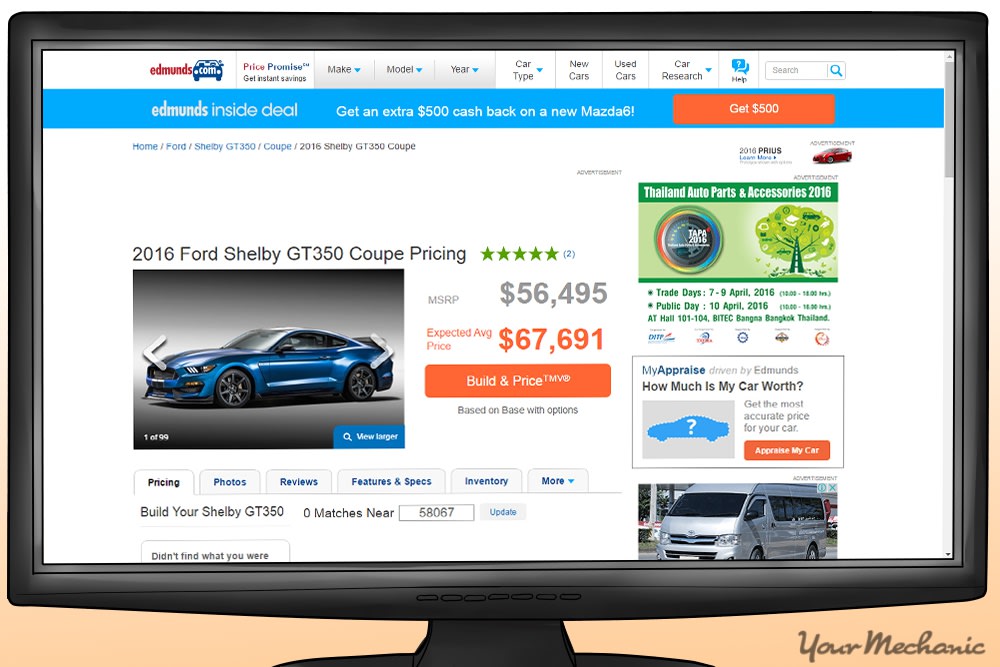

Step 4: Use the dealership's Internet department: You can also shop through the dealership's Internet department.

Using a site such as Edmunds.com, you can send requests for price quotes from the Internet managers at different local dealerships at the same time.

After receiving the price quote, follow up with an email request for a lease quote.

This allows you to easily compare lease prices from different dealerships.

Step 5: Come prepared: Regardless of your credit rating, it always pays to be prepared when leasing a car.

Research the vehicle you are interested in and pull up Kelley Blue Book values so you know what is a fair price to pay.

- Tip: Before finalizing a deal on a used vehicle, it pays to have a trusted mechanic inspect it so there are no surprises after you drive off the lot. If you have any doubts about the vehicle condition or the deal, keep looking.

Step 6: Shop your financing: Dealerships and their financing partners are not the only sources for car loans.

This is especially true for car lessors with poor credit ratings. Lenders that specialize in “subprime” loans may be a more affordable solution. Shop your loan with these lenders to see what is available to you.

- Tip: Remember, there are other options. A car dealer that uses your credit score to put you in a bad deal is not someone you want to be in business with. Never accept an offer you are not happy with or that is unaffordable for you.

Part 4 of 4: Consider other alternatives

If you just can’t find a deal that makes financial sense, you may want to consider other options. Whether it’s assuming a lease, buying a car from a friend or family member, or taking public transportation for a while longer, thinking outside the box may be necessary.

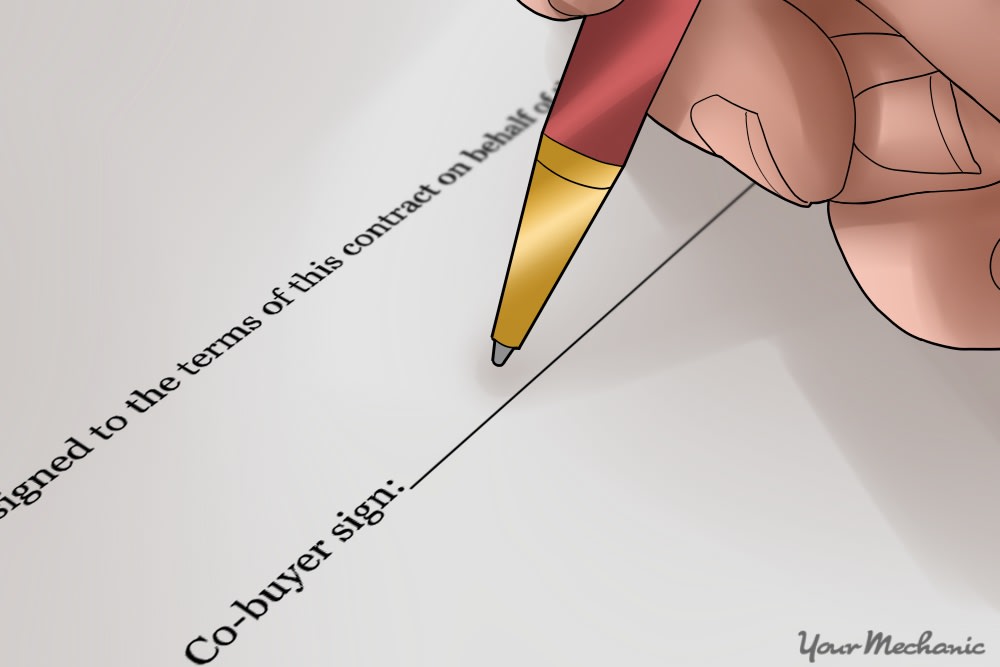

Alternative 1: Find a co-signer: This can be a tricky option.

A co-signer is someone who has a decent credit rating and is willing to co-sign your loan. The co-signer could be a friend or family member.

Keep in mind, this puts them on the hook for the payments if you fail to make them. So, it is not an agreement that should be entered into lightly by either party.

To qualify as a co-signer for a leased vehicle, someone needs:

A credit score of at least 700 or better.

Proof of their ability to play, including pay stubs or wage vouchers, or tax returns for self-employed co-signers.

A stable residence and employment history. Just like the person signing up for the lease, lenders prefer co-signers who have lived and worked in one location for a long period of time.

Alternative 2: Assume a lease: It is possible to take over an existing lease.

This is called a lease transfer or lease assumption.

Basically, you take over the leasing payments for someone that needs to get out of a car lease.

While your credit will be checked, the requirements are not as stringent as a car loan or new lease. Check Swapalease.com to see leases available in your area.

Alternative 3: Improve your credit score: The truth is that improving your credit score is not a quick and easy process but it can be done.

Paying your bills on time should be your number one priority.

A few other ways to improve your rating include:

Paying down your largest credit card balances. The difference between your balance and card limit is a big factor in your score.

Opening a new credit card account and pay the balance off every month. This shows you can be responsible with credit and will boost your score.

Tip: If you have an extremely low credit score, consider a secured credit card. These cards require a security deposit but they can be very helpful in rebuilding seriously damaged credit.

Leasing a car with a poor credit rating is difficult, but it can be done. It will require research, shopping, and patience to find a deal that works for you and your budget. Once you have made a deal and are headed off the lot, all of the work will be well worth it.