Usually, you won’t have the full payment on hand when the time comes to buy a car. Car loans exist to help you purchase a vehicle through funds borrowed through a lending facility or bank. You can get a car loan whether you are buying a new car from the dealership, a vehicle from a used car lot, or a used vehicle through a private sale.

While it can be easy just to accept whatever terms are first presented to you for financing because you are excited about your new car, you can save yourself quite a bit of money if you compare car loan interest rates as well as terms of repayment. And for those with bad or no credit, it's helpful to know your lending options.

Part 1 of 4: Set a budget for your car loan payments

When you buy a car, you need to know from the beginning how much you are able to spend on a vehicle.

Step 1: Determine how much money you have available for your car payments. Consider all of your other financial obligations including rent or mortgage payments, credit card debt, phone bills, and utility payments.

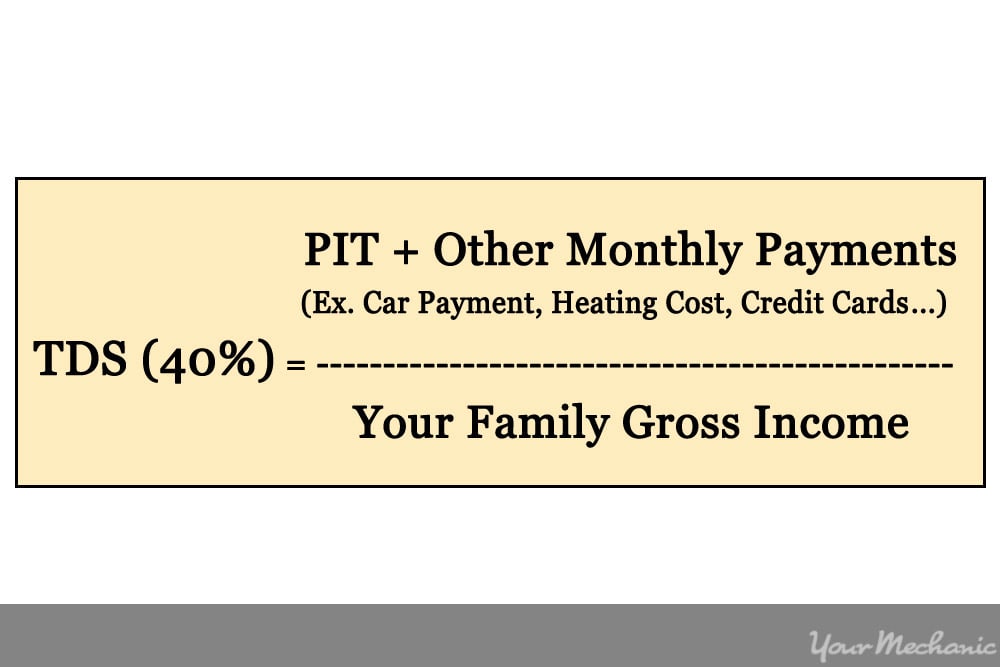

Your lender may have a total debt service ratio calculation to determine how much of your income you can spend on your car payment.

Step 2: Choose a payment schedule. Determine if you want to pay weekly, bi-weekly, semi-monthly, or monthly for your car loan.

Some lenders may not offer every option.

- Tip: If you have other bill payments scheduled for the first of every month, you may want to pay your car payment on the 15th of every month for financial flexibility.

Step 3: Determine how long you want to pay for your new car. Some lenders offer options for your new or used car purchase up to seven or even eight years.

The longer the term you choose, the more interest you will pay over the length of the term - for example, you may be eligible for a zero-interest loan for a three-year term, but a six or seven year term may be 4%.

Part 2 of 4: Determine the best financing option for a new car purchase

When you buy a new car from the dealership, you have a world of opportunities when it comes to your financing options. Finding your way through the mix doesn’t have to be confusing.

Step 1: Ask for repayment options. Request alternative repayment terms from your salesperson or finance agent.

You’ll be presented with one or two options for your car loan repayment terms, but the options may not always be the most beneficial for your situation.

Ask for longer term lengths and alternate repayment schedules.

Step 2: Ask for rebates and savings. Request information about cash purchase rebates and non-subsidized loan rates.

New car loans often have a subsidized interest rate, meaning the manufacturer uses a lender to offer interest rates lower than most banks can offer, even down to 0%.

Most manufacturers - especially when it’s close to model year-end - offer large cash purchase incentives to buyers, enticing them to buy their product.

Pairing a cash rebate with a non-subsidized interest rate may yield the best payment option for you with the least amount of interest paid.

Step 3: Find out the full cost of your new car. Ask for the total amount paid over the length of each term you are considering.

Many salespeople are hesitant to show you this information because the purchase price with interest is significantly higher than the sticker price.

Compare the total amount paid for each term. If you can make the payments, choose the term that offers the lowest overall amount paid.

Step 4: Consider using a lender apart from the car dealer. Car dealers use lenders with good rates in most cases, but you can usually achieve better rates outside of the dealership - especially through a line of credit.

Use your lower rate you obtained from your own lending institution in combination with the cash rebate from the dealership as an option that may have the best repayment terms overall.

Part 3 of 4: Determine the best interest rate for your used car purchase

Used car purchases don’t qualify for a manufacturer’s subsidized lending rates. Often, used car finance rates can be higher than new car rates along with shorter repayment terms because they are a slightly more risky investment to your lender. You can shop around for the best interest rate for your used car purchase, whether you are buying from a car dealer or as a private sale.

Step 1: Get pre-approved from your financial institution for a car loan. Obtain your pre-approval before you make a sales agreement for a used car.

If you have been pre-approved, you can confidently negotiate for a better rate elsewhere knowing that you can always fall back on your pre-approved loan amount.

Step 2: Shop for a better interest rate. Check for local lenders and banks that advertise low interest rate loans.

Don’t apply for a loan unless the terms of the loan are agreeable and better than your initial loan pre-approval.

- Tip: Shop for low-interest loan rates only from recognizable, respected lending facilities. Wells Fargo and CarMax Auto Finance are good choices for reputable used car loans.

Step 3: Make your sales agreement. If you are buying a car through a private sale, get the loan financed through the institution with the best rate.

If you are buying through a car dealer, compare the rates they can offer you with the interest rate you’ve already obtained elsewhere.

Choose the option that has the lower payments and lowest overall loan repayment amount.

Part 4 of 4: Find options for a non-prime auto loan

If you haven’t had a credit card or loan before, you will need to begin building your credit before you are going to get the prime interest rate offered. If you have a poor credit rating because of bankruptcy, late payments, or repossessions, you’re considered a high-risk customer and won’t receive prime rates either.

Just because you can’t get prime interest rates doesn’t mean you can’t get a competitive interest rate for a car purchase. You can check with several lenders to get the best terms available for your situation.

Step 1: Contact your primary financial institution for a car loan. It’s always best to start with a lender that knows your history, even if it is limited or flawed.

Get a pre-approval, knowing your interest rate will be considerably higher than their advertised rates.

Step 2: Check with other non-prime lending facilities.

- Note: Non-prime refers to a higher-risk or unestablished customer who poses a higher threat of non-payment for their loan. Prime lending rates are given to those with a proven track record of consistent and prompt payments, who are not viewed as a risk to default on their payments.

Search online for “same day car loan” or “bad credit car loan” in your area and look through the top results.

Find lenders with the best rates and contact them or fill out an online application for a pre-approval.

If the rate given is better than your pre-approval and you qualify for the loan, submit an application.

- Tip: Avoid submitting multiple car loan applications. Each application checks your credit rating with a credit bureau such as Experian, and multiple hits within a short period of time can raise red flags that result in a denial of your application.

Apply only to the best of the lenders you have inquired from.

Step 3: Check for in-house financing from your car dealer. If you are buying a car from a dealership, there may be the option to pay for your car loan in-house instead of through a lender.

In this form of loan repayment, the dealership essentially acts as their own bank. This may be your only option if you have been denied a car loan everywhere else.

Shopping for a car loan isn’t the most fun part of buying a car, but it is important to make sure you aren’t paying more than necessary for your car. Doing some research and being prepared can get you the best repayment option, and can also help you to put down a large down payment on your car purchase, motivating the lender to work with you even harder.