If it’s time to replace your current vehicle, it’s a good idea to look at all of your buying options, and leasing is one option you should definitely consider.

A lease lets you drive off the lot in a brand new vehicle without dropping a big down payment (20 percent is typical on a car loan) or having to take out a car loan at all. As an added benefit, leasing allows you to drive a new vehicle that is under warranty and will usually not require any major repairs.

Lease payments also tend to be lower so you can afford a more luxurious vehicle and a higher trim level.

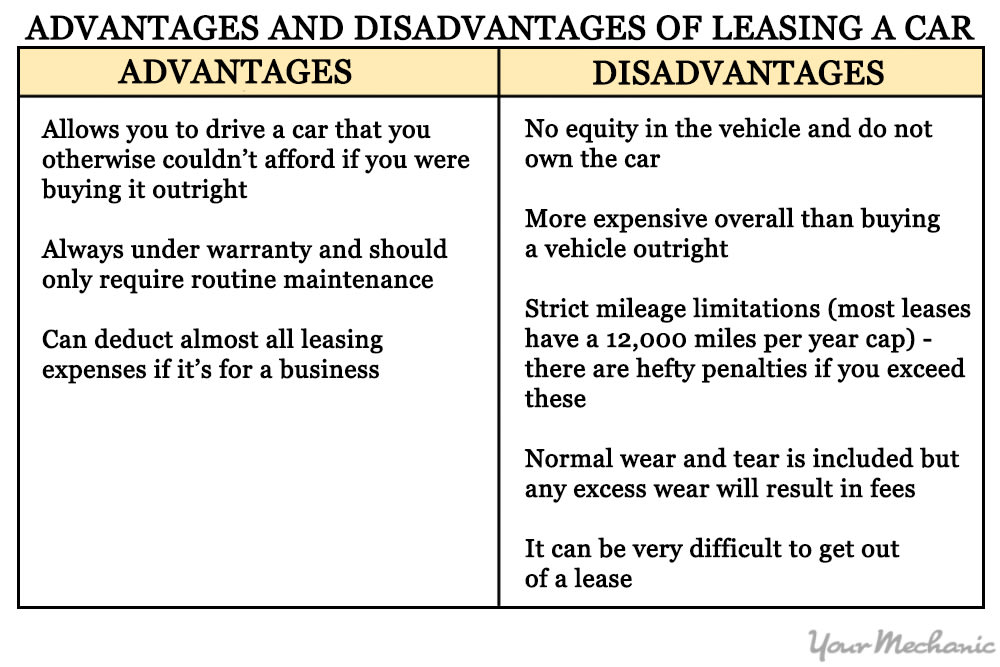

While there are many benefits of leasing, there are downsides as well and leasing is not for everyone. Understanding the leasing process and the advantages and disadvantages are key to successfully leasing a vehicle.

The following are detailed steps on how to lease a new vehicle as well as all of the pitfalls you should be aware of before signing on the dotted line.

Part 1 of 3: Understanding leasing and setting a budget

Step 1: Determine if leasing is right for you. Understanding the process of leasing is essential to making the right decision.

First, it is important to understand the basics of how leasing works:

In most cases a small down payment is required. The dealer will usually refer to this as the “due at signing” number. This number can range from zero to a few thousand dollars depending on the vehicle you are leasing.

Leases have terms — the number of months for which you must make lease payments — ranging from 12 to 48 months. The most common terms are 24 and 36 months.

When the lease term ends you simply return the vehicle to the dealer or leasing company. It is also possible to purchase the vehicle if you decide to keep it.

Next, it is imperative to consider the advantages and disadvantages that come with leasing a car.

Step 2: Set a budget. Once you’ve decided that you would in fact like to lease your next car, you will need to set your budget.

Do this before you even start looking at vehicles. Take a hard, long, and very realistic look at your finances and determine how much you can afford for both a monthly lease payment and a down payment.

Step 3: Consider lease terms. While a longer lease term will lower your monthly payment, most experts recommend limiting the lease term to 36 months. This way the vehicle is under warranty for the entirety of the lease.

Step 4: Determine your mileage limits. A standard lease usually sets the mileage limit at 12,000 miles per year. It is possible to up the mileage limits, but this will increase the monthly payment. Be realistic as mileage overages can be expensive.

Step 5: Consider insurance payments. Don’t forget to get an insurance quote to factor into your budget. A lease requires full coverage on the vehicle at all times.

Part 2 of 3: Finding a vehicle

Leases are available on most vehicles. Research and test-drive a number of vehicles to determine which ones you are interested in leasing. A few things to consider:

Maintenance costs can be pricey, especially on luxury vehicles. Because you will be responsible for routine maintenance costs, it pays to research vehicle reliability and the cost of routine maintenance.

When searching for a vehicle, do not mention that you are interested in leasing.

Step 1: Search online for leasing deals or rebates. Automakers often offer discounted leasing specials. Details are usually available on the manufacturer’s website. Be sure to read the fine print in regards to fees and taxes.

Step 2: Shop around for the best deal. Contact a number of dealers for a price quote on the vehicle you want. Make sure you are comparing identical vehicles when getting quotes.

- Tip: Negotiating the final purchase price before you mention leasing will result in a better deal.

Step 3: Get your initial financing in order. Make sure you can afford the “due at signing” payment. This number will be detailed on the manufacturer's website if you are shopping dealer specials.

For any vehicles you are interested in leasing, you will need to determine how much you can afford as a down payment. Review your budget carefully, and use a leasing calculator to determine how much of a down payment you will need to make your lease affordable.

If you will require a loan to cover this amount, arrange financing before going to the dealership. Check with local banks that you already have relationships with as well as financing companies and credit unions. Talk to a loan officer regarding your circumstances and ask him or her to explain your loan options. When you have decided the amount and type of loan that you are interested in, shop around to get the best interest rate.

Part 3 of 3: Making a deal

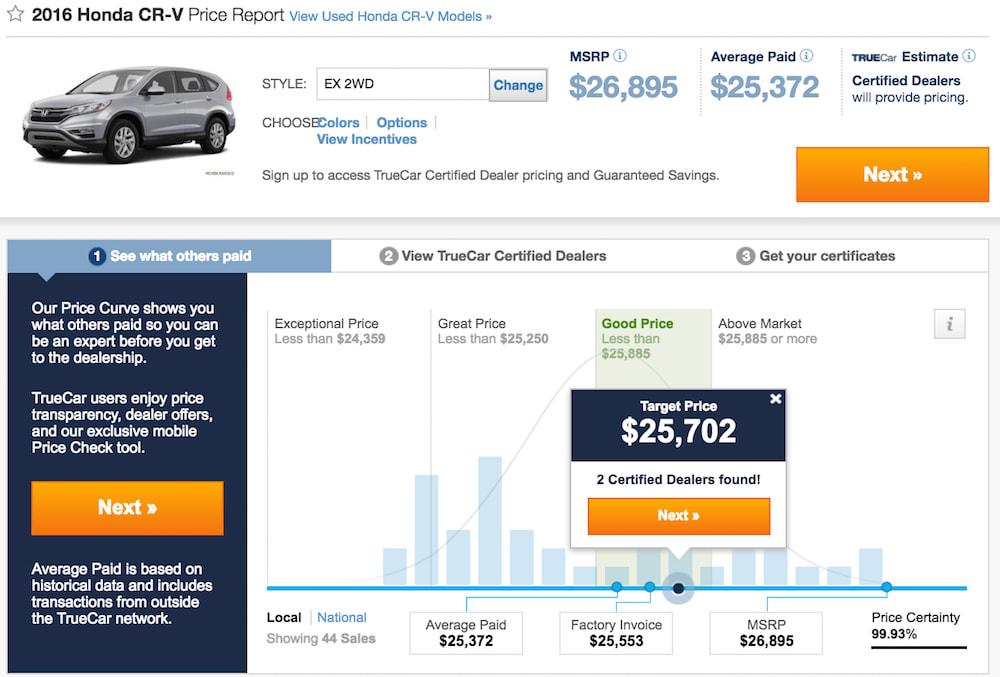

Step 1: Look up the value of the car. Use sites such as Truecar and Edmunds to get an idea of how much the specific vehicle you are interested in is selling for in your area before you head into the dealership.

Set a target price for the car and be ready to negotiate to get that price.

Step 2: Negotiate the purchase price. Head to the dealership of your choice to negotiate the price. Do not mention you are looking to lease when first talking with the salesperson.

The cost of your lease will depend on the negotiated purchase price for the vehicle. The better price you get on the car, the lower your lease payment will end up being, so your first priority is to work out the best deal you can on the vehicle price.

Here are a few negotiating tips:

- Be prepared, know the details about the vehicle you want as well as any options and trim levels.

- Have quotes from other dealers ready to show the salesperson.

- Have a target price in mind.

- Eat before heading to the dealership. Buying a vehicle can be a lengthy process and if you are hungry you may cut corners to get the deal done faster.

- Be prepared to walk out if you don’t like the deal.

Step 3: Negotiate the leasing terms. When you have agreed upon a purchase price, it's time to talk leasing terms.

Here are a few leasing terms you should be aware of before you sit down at the negotiating table:

Capitalization cost (cap cost): This is the total price of the car, which includes the price you negotiated along with any taxes and dealer fees. The lessor (the car dealer) uses this amount to calculate your monthly payment.

Cap Reduction: This is the down payment you will be giving to the dealer. The more money you put down, the lower your monthly lease payment end up being. It is also possible to apply the value of any trade-in you may have to the cap reduction.

Your first step is to work out the term of the lease and the mileage allowance. If you think you will be using more than the allotted miles per year, negotiate a higher mileage allowance, but remember, this will increase your monthly payment.

Then negotiate the cap reduction. The more money you put down, the lower your lease payment will end up being. If the manufacturer is offering any rebates, make sure they are applied as a cap reduction.

Step 4: Understand the residual value. An important component of any lease is the residual value. This is the amount that the car will be worth when the lease ends.

Residual values have a big impact on your payment and are set by lending companies based on historical data. In most cases the residual value is not negotiable.

In order to calculate the lease payment, the lender takes the negotiated price of the car and subtracts the residual value, which gives them the vehicle value you will be using up over the term of your lease.

As an example, if the price of the car is $35,000 and the residual value is $20,000 after a three-year lease, you are using up $15,000 worth of the vehicle's value over the term of your lease. This works out to a $416-a-month payment.

A higher residual value will lead to lower monthly payments as you are using up less of the vehicle’s value, so in this sense, a higher residual value is better. But, if you end up purchasing the vehicle at lease end, a higher residual value is less desirable.

Step 5: Review the lease documents and beware of add-on fees. Before signing the lease, it is important to completely review all of the lease documents.

If you are unclear about something, be sure to ask for an explanation, and if you are not satisfied with the answer, consider walking away. Leases are legal documents so make sure you understand and are comfortable with all of the terms and conditions.

Dealers will often add in fees. All of these fees are negotiable, despite what the salesperson says. They will also vary from dealership to dealership, so when shopping, look for a dealer who avoids these fees. If the salesperson is unwilling to negotiate or eliminate them, consider going to a new dealer.

Here are some examples of potential add-on fees that you might see:

Acquisition Fee: This is also referred to as a document fee and is charged at the beginning of the lease.

Disposition Fee: This fee is charged if you return the car and do not lease or purchase a new vehicle from the dealer.

Purchase-Option Fee: This is a fee the dealer charges if you do decide to purchase the vehicle at the end of the lease. The amount of this fee can vary dramatically.

Step 6: Sign the lease. Once your are comfortable with all of the lease terms and conditions, sign the lease and drive off in you brand new car.

Leasing a vehicle is not for everyone, but if you do your research and negotiate a great price on the vehicle, leasing can be an excellent buying choice. Hopefully, you now have a solid understanding of the leasing process and will be able to work out a fabulous deal on the car of your dreams.