When you buy a new car, you’ll likely finance a large portion of your purchase. Very few people can pay for the whole amount up front. Unless you are able to obtain 0% interest on your vehicle loan, your terms of repayment will include interest on the principal amount you borrow.

The financing terms depend on your personal financial situation. If you have excellent credit, you typically are eligible for the lowest available interest rates. If your credit is poor, you may not be eligible for a car loan or may have to pay high interest rates. If you have very little credit experience, you may not be able to get car financing or may be required to pay high interest rates.

In any situation, you’ll want to save as much money as possible. While your personal car isn’t eligible to be a tax-deductible expense, there is a way to claim the interest on your car loan as a tax-deductible expense.

Whether you have good credit, bad credit, or no credit, if you have equity in your house, you can turn the interest you pay on your car loan into a tax-deductible expense.

Part 1 of 3: Obtain a home equity line of credit

A home equity line of credit, also known as a HELOC, uses the equity you have in your home as a source to borrow from through your lender.

Step 1: Determine available equity. The amount of equity you have in your home is the amount your home is worth in the current housing market minus what you owe on the property.

Usually, a HELOC will only finance up to 80% of your home’s value minus what you owe on the property.

For example, if your home is worth $200,000 in the current market and you owe $120,000 on your mortgage, you have $80,000 equity in your home. If your lender only finances 80% of your home’s value, which is $160,000, then your available HELOC amount is $40,000, which is the difference between what you owe and 80% of your property’s market value.

Step 2: Consider your options with your lender. Discuss the options you have for a home equity line of credit with your lender.

Once you obtain the line of credit, you can begin the process of purchasing a car with tax-deductible interest.

Part 2 of 3: Purchase a vehicle with your home equity line of credit

Step 1: Make a sales agreement. Draw up a sales agreement with the car dealership to purchase your desired car.

The sale amount will be paid in full if you are using your home equity line of credit, so you have more negotiating power with the salesperson to get the best deal.

- Tip: If you are not using the dealer’s financing options, often you are eligible for cash rebates of several thousand dollars, especially if the model year-end is nearing. Take advantage of cash rebates to further lower the sale price.

Step 2: Use your HELOC for payment. Complete the sale with payment from your HELOC.

Get a check or bank draft for the sale amount from your lender for the full sale amount. You can only claim the interest on the amount paid from your HELOC.

- Warning: If you use a home equity line of credit for your car purchase, you need to be aware that your home is the primary asset on the loan, not the car. If you default on the line of credit payments, your house could be seized by your financial institution.

Part 3 of 3: Claim your car payment interest on your income tax

Step 1: Determine the interest paid on your HELOC for the year. Add the interest payments noted on your monthly statements to get the total for the year.

You can also contact your financial institution for a summary of the account.

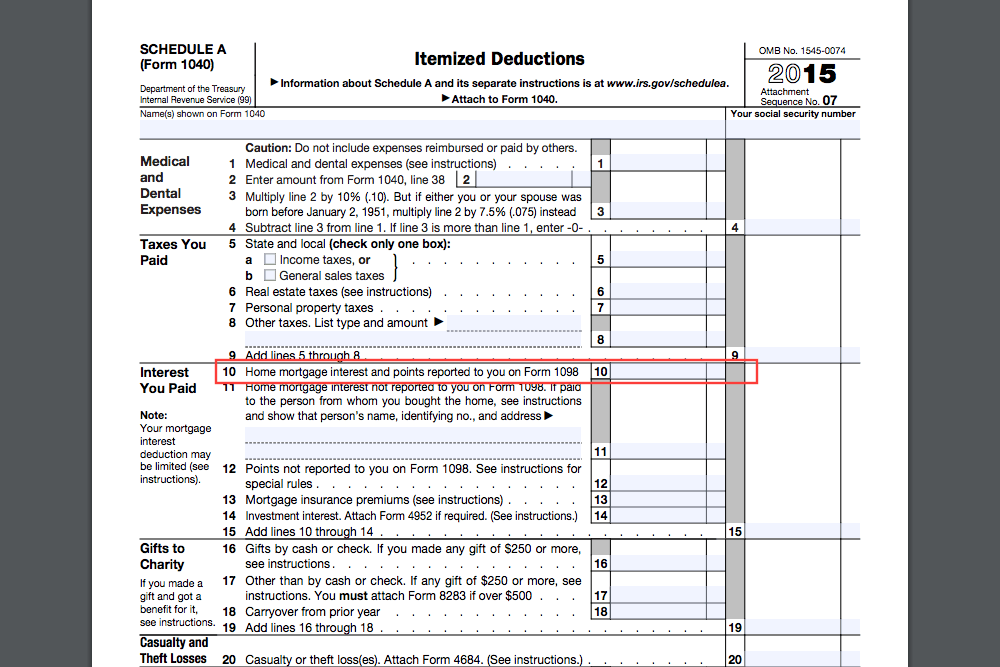

Step 2: Fill out tax document. Complete Form 1040 Schedule A for your income tax return.

Schedule A is the form where you record your deductions for the year. Fill your interest amount from your HELOC on line 10 of the form.

If there are other amounts you need to claim on line 10, “Home mortgage interest and points reported to you on Form 1098,” add them together. Your bank is required to file Form 1098 to the Internal Revenue Service for the interest received on your mortgage, so be sure your numbers are accurate.

- Warning: Mismatched information can result in delays processing your tax return and even penalties for filing a fraudulent tax return.

Step 3: Submit your tax return to the IRS including Schedule A. You may need to file your supporting documentation for interest paid if requested by the IRS.

Before purchasing a car through a Home Equity Line of Credit for the purpose of claiming the interest as tax-deductible, check with your accountant or tax professional to make sure it is legal for your situation, and have one of YourMechanic’s certified professionals perform a pre-purchase inspection to make sure the car is in great shape.