Sometimes, it can be challenging to apply for a car loan while in the military. With changing assignments and short-notice deployments, some lenders are wary of selling to members of the military.

However, members of the military have other avenues of obtaining the financing they need to purchase a vehicle. Members of the armed forces can gain access to affordable and flexible car financing by applying for an auto loan through one of the many military-friendly banks and credit unions.

Part 1 of 5: Open an account

The first step in acquiring a car loan as a member of the military is to sign up at a bank that caters to military members. Institutions such as USAA Bank, Navy Federal Credit Union, and Armed Forces Bank offer a variety of services, including low APR auto loans.

Step 1: Check out different offerings. Before signing up for an account, check to see the annual percentage rates and terms that the bank offers.

While many military-friendly banks and credit unions are known for their affordable rates, you should still make sure their rates and terms are what you are looking for.

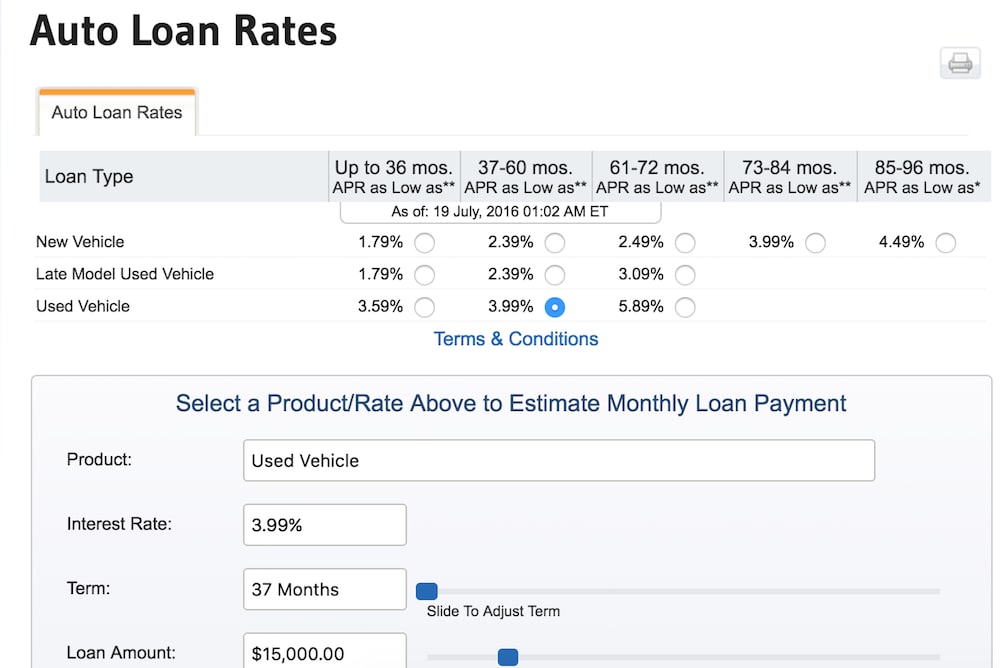

Step 2: Use an online auto loan calculator. By using the tools provided at one of the military-friendly financial institution websites, you can determine how much you should expect to end up paying over the lifetime of the loan.

Navy Federal Credit Union offers a helpful calculator to help you determine how much you have to pay depending on the APR amount, the length of the loan, and whether you get gap insurance or not.

Step 3: Gather the necessary paperwork. In order to qualify for an account at one of the military-friendly banks or credit unions, you must first of all be a member of the armed forces, an honorably discharged former member of the military, or a military spouse or other family member.

In addition to this, you also need to provide the following documentation:

- Social security number (SSN)

- Driver's license or government ID

- Current home address

- Current email address

- Credit card or bank account routing number (to fund your account with an initial deposit to open your account)

Part 2 of 5: Check your credit

Once you have signed up for an account at a military bank or credit union, you need to make sure you have a decent credit score. There are a few ways in which you can get a credit report, including getting one for free or paying for one from one of three credit reporting agencies – Equifax, Experian, and TransUnion.

Step 1: Get a free credit report. You are entitled to a free credit report from each of the three credit reporting agencies once a year.

To receive a free credit report, you can go to AnnualCreditReport.com to request a report.

- Tip: Keep in mind though that the free annual credit reports you receive do not include your actual credit score. To get your credit score, you can either check your credit card statement (some major credit card companies provide this service), talk to a non-profit credit counselor, use a credit score service, or pay one of the credit reporting companies to get your score. You can pay to access your score at myfico.com.

Step 2: Repair your credit. Once you know where you stand with your credit report and have identified any discrepancies, it is time to clear up any inaccuracies.

If you find something that is not correct on your credit report, you can dispute it and try to get the reporting agency to remove the inaccuracies. Keep in mind that disputing an item is not always successful.

Other ways to repair your credit include paying your bills on time and signing up for a secured credit card with a small balance, and then using the card and paying it off each month over the course of a few months or longer. This should help you establish credit and build your credit score back up.

Part 3 of 5: Apply for a loan

After you repair your credit, it is time to apply for an auto loan. You can either perform this process in person or online.

Step 1: Apply for a loan. When you apply, the lender will submit a series of questions for you to answer.

- Note: Answer each question as accurately as you can. The information you give is subject to validation, and if you fail this process, the financial institution can reject your application for an auto loan.

Once you have submitted your loan application and answered the questions presented, it usually takes at least one business day to receive a response, or sooner if you have good credit and income.

Step 2: Provide all necessary documentation. You may need to provide some additional documentation apart from the completed the loan application form.

The documentation you need to provide includes:

- Driver's license or government-issued ID

- Social security number

- Proof of income

- Proof of insurance

If you plan on making a down payment, you will need to get it ready before the lender can complete the loan-approval process.

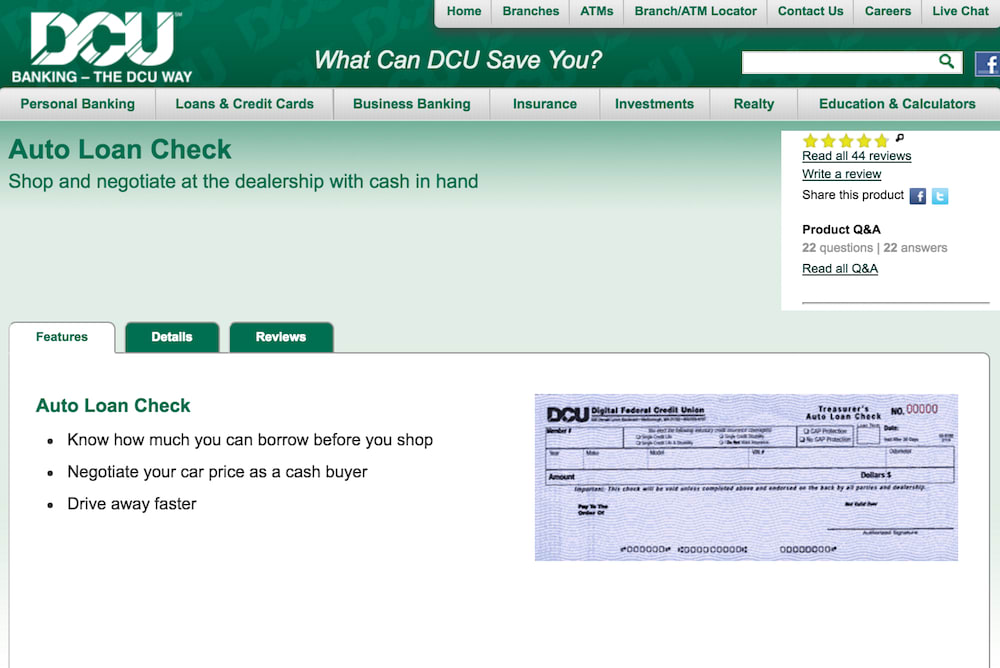

Step 3: Receive a check. If you are approved, the bank issues a "blank check" that is good for a predetermined amount.

You will need to give this document to the dealership when you go to buy a vehicle. The dealership then works with the lender to finalize the auto loan process.

Part 4 of 5: Select a vehicle that qualifies for a loan

Now that you have received approval from the lender in the form of a check for a certain amount, it is time to find a vehicle. Before purchasing a vehicle, first make sure it meets all of the lender's requirements.

Step 1: Check lender requirements. Banks and credit unions usually impose some criteria to finance a vehicle. Some of the more common criteria include the vehicle's age, condition, and mileage.

When it comes to mileage, many lenders prefer a vehicle that has between 75,000 to 100,000 miles at most. This means that for a used car, lenders prefer vehicles between seven and eight years old.

Step 2: Check credit score requirements. Your credit score can also play a part in how much you can get financed. Lenders usually only finance amounts that are up to six to 10 times your monthly income.

Financial experts recommend that you spend no more than 50 percent of your yearly income on a vehicle, and this figure includes any down payment you make for it.

Step 3: Select a vehicle. After you have determined what vehicles the lender is willing to finance and how much you are willing to have financed, it is time to choose a vehicle.

Follow the usual procedures when shopping for a vehicle, including:

Looking up the fair market value of any vehicle you are interested in. Some sites for this include Kelley Blue Book, Edmunds, and Cars.com.

Check out the vehicle's history. If the dealership doesn't offer a free vehicle history report, check out Carfax, or another similar service, to purchase your own report.

Finally, take the vehicle on a test drive. While on the test drive, have a trusted mechanic check the vehicle for any problems.

Part 5 of 5: Purchase the vehicle

The last step in the car-buying process is to purchase the vehicle. You must sign all of the paperwork and register the vehicle in your name, making sure to pay any taxes and associated fees in the process. The lender holds onto the vehicle’s title until you pay the auto loan amount in full.

Step 1: Sign the paperwork. Once you are satisfied with the vehicle and the price set by the dealership, it is time to sign the documentation.

You should receive a copy of any documentation you sign, including the bill of sale. When purchasing a new or used vehicle, you should receive copies of other documents like the odometer mileage disclosure form, vehicle registration, and a lemon law rights statement in some states while buying a new vehicle.

Step 2: Pay taxes and registration. Usually this amount is included in the sale price of the vehicle. Make sure that you have paid all necessary taxes and fees before you leave the dealership.

The dealership should receive your license plates within a few weeks of buying your vehicle and will notify you to come and pick them up.

If you register the vehicle on your own, you may receive your plates on the day of registration.

Buying a new or used vehicle in the military is easy if you know how to take the right steps. By registering an account at a military-friendly bank or credit union, you can take advantage of the low APRs that they offer. Such institutions also work with members of the military and understand the hardships involved, such as deployment and changes of duty assignment.

Before purchasing a vehicle, have one of our expert mechanics perform a pre-purchase car inspection to make sure that the vehicle you plan on buying is in perfect working order.